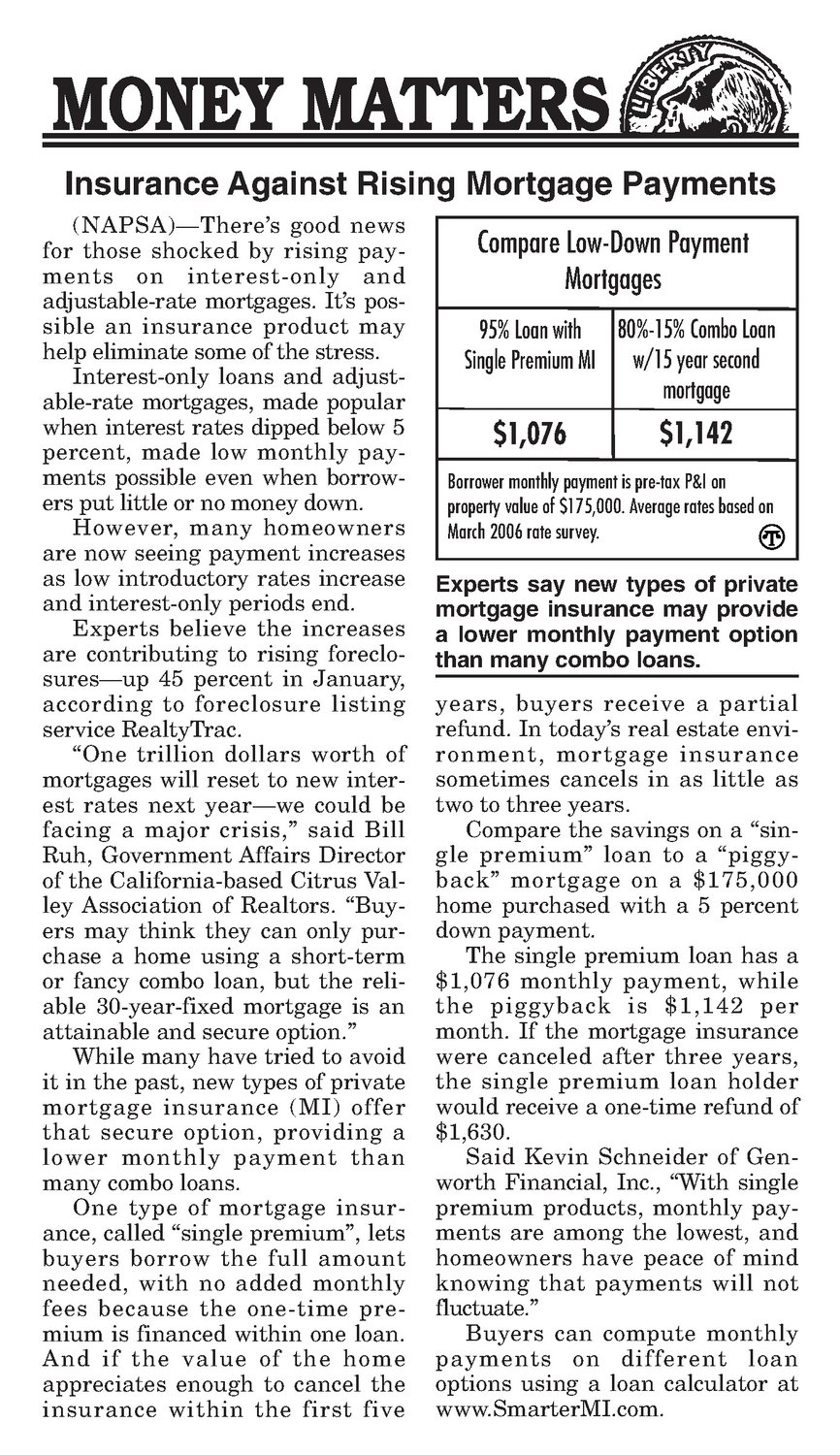

Insurance Against Rising Mortgage Payments (NAPSA)—There’s good news for those shocked by rising payments on interest-only and adjustable-rate mortgages. It’s possible an insurance product may help eliminate someof the stress. Interest-only loans and adjustable-rate mortgages, made popular when interest rates dipped below 5 percent, made low monthly payments possible even when borrowers putlittle or no money down. However, many homeowners are now seeing payment increases as low introductory rates increase and interest-only periods end. Experts believe the increases are contributing to rising foreclosures—up 45 percent in January, according to foreclosure listing service RealtyTrac. “One trillion dollars worth of mortgages will reset to new interest rates next year—we could be facing a majorcrisis,” said Bill Ruh, Government Affairs Director of the California-based Citrus Valley Association of Realtors. “Buyers may think they can only purchase a home using a short-term or fancy combo loan, but the reliable 30-year-fixed mortgage is an attainable and secure option.” While manyhavetried to avoid it in the past, new types of private mortgage insurance (MI) offer that secure option, providing a lower monthly payment than many comboloans. One type of mortgage insurance, called “single premium”, lets buyers borrow the full amount needed, with no added monthly fees because the one-time premium is financed within one loan. And if the value of the home appreciates enough to cancel the insurance within the first five Compare Low-Down Payment Mortgages 95% Loan with —|80%-15% Combo Loan Single Premium MI w/15 year second mortgage $1,076 $1,142 Borrower monthly paymentis pre-tax P&l on property value of $175,000. Average rates based on March 2006rate survey. QD Experts say new types of private mortgage insurance may provide a lower monthly payment option than many comboloans. years, buyers receive a partial refund. In today’s real estate environment, mortgage insurance sometimes cancels in aslittle as two to three years. Compare the savings on a “single premium” loan to a “piggyback” mortgage on a $175,000 home purchased with a 5 percent down payment. The single premium loan has a $1,076 monthly payment, while the piggyback is $1,142 per month. If the mortgage insurance were canceled after three years, the single premium loan holder would receive a one-time refund of $1,630. Said Kevin Schneider of Gen- worth Financial, Inc., “With single premium products, monthly payments are among the lowest, and homeownershave peace of mind knowing that payments will not fluctuate.” Buyers can compute monthly payments on different loan options using a loan calculator at www.smarterMI.com.