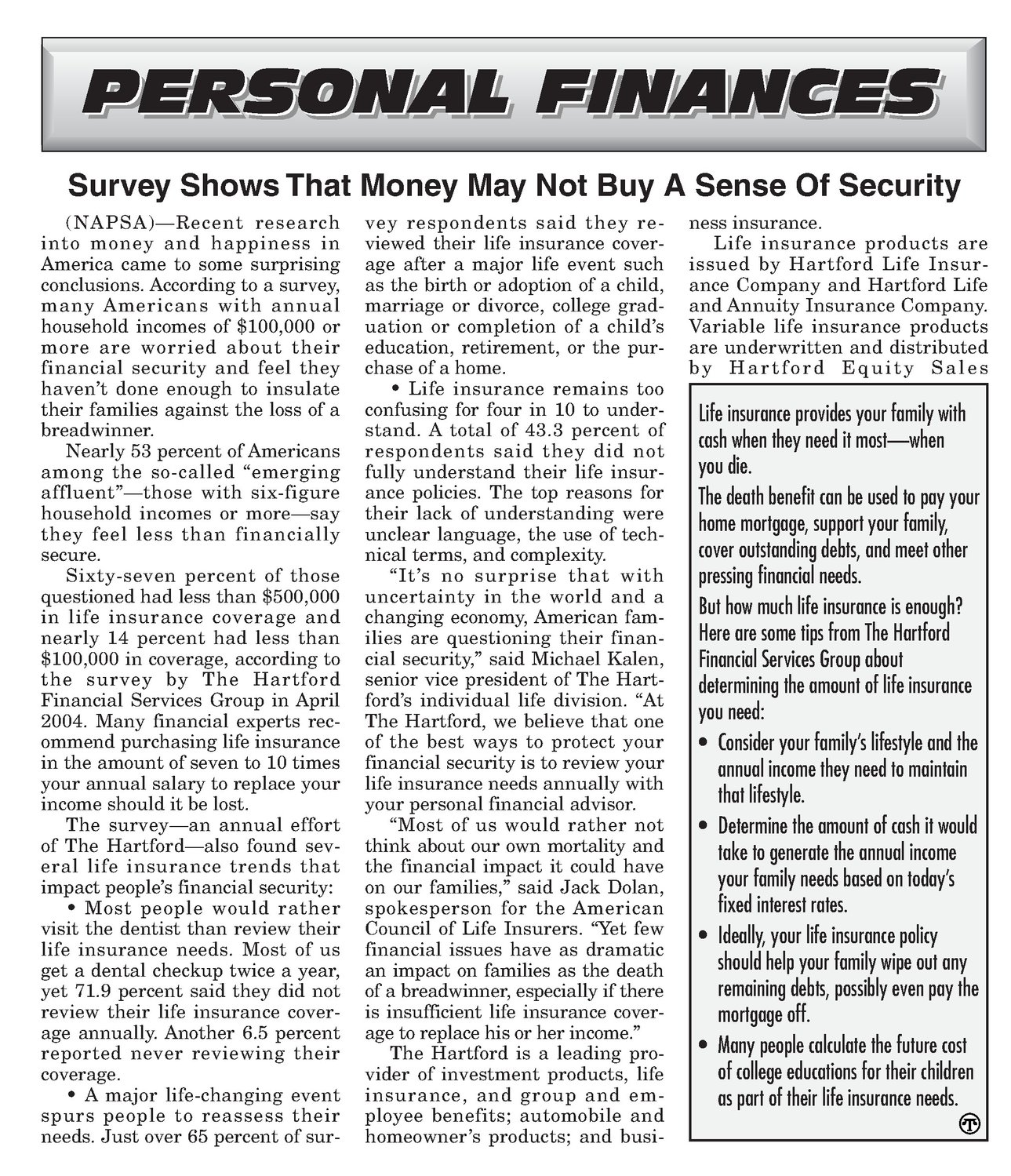

Survey ShowsThat MoneyMay Not Buy A Sense Of Security (NAPSA)—Recent research into money and happiness in America came to some surprising conclusions. According to a survey, many Americans with annual household incomes of $100,000 or more are worried about their financial security and feel they haven’t done enough to insulate their families against the loss of a breadwinner. Nearly 53 percent of Americans among the so-called “emerging affluent”—those with six-figure household incomes or more—say they feel less than financially secure. Sixty-seven percent of those questioned hadless than $500,000 in life insurance coverage and nearly 14 percent had less than $100,000 in coverage, according to the survey by The Hartford Financial Services Group in April 2004. Manyfinancial experts recommend purchasinglife insurance in the amount of seven to 10 times your annualsalary to replace your income shouldit be lost. The survey—an annualeffort of The Hartford—also found several life insurance trends that impact people’s financial security: Most people would rather visit the dentist than review their life insurance needs. Most of us get a dental checkup twice a year, yet 71.9 percent said they did not review their life insurance coverage annually. Another 6.5 percent reported never reviewing their coverage. A major life-changing event spurs people to reassess their needs. Just over 65 percent of sur- vey respondents said they reviewed their life insurance coverage after a major life event such as the birth or adoption of a child, marriage or divorce, college graduation or completion of a child’s education, retirement, or the purchase of a home. Life insurance remains too confusing for four in 10 to understand. A total of 43.3 percent of respondents said they did not fully understand their life insurance policies. The top reasons for their lack of understanding were unclear language, the use of technical terms, and complexity. “Tt’s no surprise that with uncertainty in the world and a changing economy, American fam- ilies are questioning their financial security,” said Michael Kalen, senior vice president of The Hartford’s individual life division. “At The Hartford, we believe that one of the best ways to protect your financial security is to review your life insurance needs annually with your personalfinancial advisor. “Most of us would rather not think about our own mortality and the financial impact it could have on our families,” said Jack Dolan, spokesperson for the American Council of Life Insurers. “Yet few financial issues have as dramatic an impact on families as the death of a breadwinner, especially if there is insufficient life insurance coverage to replace his or her income.” The Hartford is a leading provider of investment products, life insurance, and group and employee benefits; automobile and homeowner’s products; and busi- ness insurance. Life insurance products are issued by Hartford Life Insurance Company and Hartford Life and Annuity Insurance Company. Variable life insurance products are underwritten and distributed by Hartford Equity Sales Life insurance provides your family with cash whenthey need it most—when you die. The death henefit can be used to pay your home mortgage, support your family, cover outstanding debts, and meet other pressing financial needs. But how much life insurance is enough? Here are sometips from The Hartford Financial Services Group about determining the amount oflife insurance you need: Consider your family’s lifestyle and the annualincome they need fo maintain thatlifestyle. Determine the amount of cash it would take to generate the annual income yourfamily needs based on today’s fixed interest rates. e Ideally, yourlife insurance policy should help your family wipe out any remaining debts, possibly even pay the mortgageoff. e Many people calculate the future cost of college educationsfor their children as part of their life insurance needs. @